Last two months have been one of the most disrupted phases for India’s mouldmakers, and the turbulence in the availability of engineering plastic granules shows no sign of easing. Plastic granules, being a petroleum by-product, have seen sharp price increases. The shortages and price volatility are rippling across MSMEs, automotive suppliers, and consumer goods manufacturers. Shipping delays, container shortages, and unpredictable crude oil movements have all intensified due to the transit uncertainty through the Strait of Hormuz amid the US‑Iran conflict, which has compounded the crisis, leaving smaller manufacturers squeezed between rising input costs and rigid market pricing.

The strain is visible across sectors as the injection moulding industry struggles with erratic supplies and escalating costs. Over half of MSME production is partial, jobs are hit, and cash‑flow stress from freight surcharges and weekly price swings is mounting. With tooling demand shrinking and projects stalled, recovery depends on supply chain stability and easing cost pressures.

What are Engineering Plastics

Engineering plastics are high-performance polymers designed for superior mechanical, thermal and chemical properties compared to standard plastics. They offer excellent strength, durability and resistance to heat and chemicals, making them suitable for demanding applications. Common types include polycarbonate (PC), polyamide (PA), polyoxymethylene (POM) and polyetheretherketone (PEEK), each tailored for specific industrial needs.

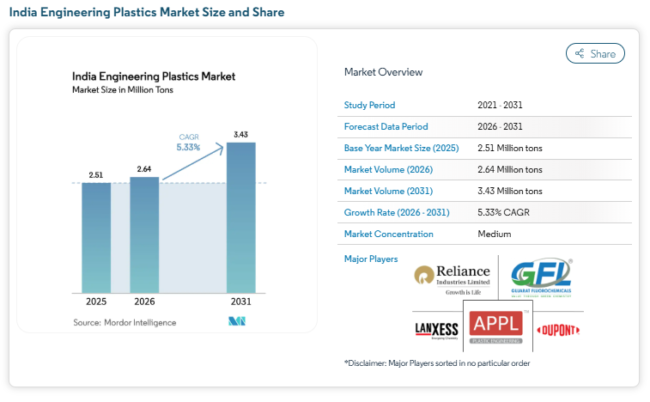

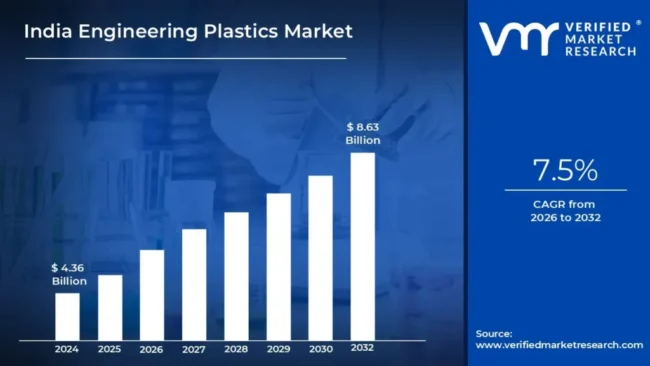

According to Mordor Intelligence (a market research and consulting firm that provides syndicated and custom industry reports, market share analysis, and 5-year growth forecasts), the Indian Engineering Plastics Market size is expected to grow from 2.51 million tons in 2025 to 2.64 million tons in 2026 and is forecast to reach 3.43 million tons by 2031 at 5.33% CAGR over 2026-2031. While Verified Market Research (a global market intelligence and consulting firm that provides syndicated research reports, data analytics, and custom consulting for niche and emerging industries) states that the rising demand for engineering plastics is enabling the market to grow at a CAGR of 7.5% from 2026 to 2032.

Source: https://www.mordorintelligence.com/industry-reports/india-engineering-plastics-market

Source- https://www.verifiedmarketresearch.com/product/india-engineering-plastics-market/

Fluctuating prices of petrochemical feedstocks and speciality chemicals are creating major challenges for India’s engineering plastics industry, impacting production costs, profit margins, and supply planning. Manufacturers are also being forced to adopt flexible material formulations and stronger inventory strategies to manage supply and price uncertainties.

MSMEs struggle with import dependence and supply prioritization

The recent disruptions in the non- availability of engineering plastic granules are significantly impacting the moulding industry, especially MSMEs involved in plastic component manufacturing, says Shijesh Kokkodan, Director, MacPro Technologies Pvt. Ltd., a Bengaluru-based company engaged in manufacturing precision molds, dies, and engineering components.

Mr. Kokkodan explained that most engineering plastics such as nylon, PBT, polycarbonate, Delrin, and PPS are almost entirely dependent on imports. Indian manufacturers rely on local dealers who stock imported materials and distribute them to MSMEs. Companies in this segment typically have turnovers ranging from ₹5 crore to ₹100 crore and consume around 5 to 15 tons of material monthly, depending on the product mix.

Uncertainty leaves mouldmakers unable to quote prices

“This is the biggest disruption we have ever seen by the Indian mould makers in the non‑availability of engineering plastic granules, and it is all because of the transit uncertainty through the Strait of Hormuz,” stressed Jayesh Rambhia, Hon. Chairman, Plastivision India, one of the world’s largest plastics industry trade fairs organized by The All India Plastics Manufacturers’ Association (AIPMA).

He further added, that, “Last year India imported 20 billion USD. There is so much uncertainty in the market today that mouldmakers are unable to quote any prices with confidence. Whatever rate is quoted today is bound to change tomorrow.”

One of the biggest challenges currently is supply prioritization. Due to shipping disruptions, container shortages, and logistics issues, manufacturers and dealers are prioritizing buyers purchasing in bulk quantities, sometimes 50 tons or more. Smaller manufacturers are often denied regular credit terms and are instead asked to make advance payments to secure material supplies.

Source- https://www.plastivision.org/aipma.php

Granule and steel costs escalate across industries

Further Arvind Chawla, Director, MEPL SiddhoHum Pvt. Ltd., explained that, “Plastic granules, being a petroleum by‑product like LPG, petrol, or diesel, have seen sharp increases in the last two months. Granules are not required for making moulds, which are made of steel, but steel prices too have risen by 15–20% due to furnace costs and dollar fluctuations. Plastic granules such as polypropylene and polyethylene, used in household products, and engineering plastics like nylon, ABS, and PVC, used in industrial and automotive applications, have gone up by 20–25%. This has hit industries across automobiles, medical, and consumer goods. While large buyers can negotiate on bulk orders, smaller quantities face even steeper hikes.”

The pricing of raw materials has become highly unpredictable, with rates changing almost every week. According to industry leaders, there is ‘no clarity or benchmark’ in pricing, and increases are often justified by citing war-related disruptions or freight issues.

In terms of price escalation, Mr. Kokkodan stated that engineering plastic prices have increased by nearly 50% for smaller-volume buyers, while larger buyers are seeing increases of around 20–25%. He emphasized that even a 5% variation can significantly affect the profitability of MSMEs because the automotive industry which is one of the largest consumers of molded plastic components operates on extremely thin margins.

Recent increases have been around 30% or even higher in some cases. For example, a material that was priced at ₹120 per kilo has gone up to ₹180 per kilo. Another material that was ₹250 per kilo has gone up to ₹300 per kilo. Materials costing ₹600 per kilo have increased to ₹700 per kilo.

The current rates of these materials typically range anywhere from around ₹250 per kilo to ₹600 per kilo depending on the grade, quality, and glass fiber composition.

For companies consuming 15–20 tons of material every month, these increases translate into several lakhs of additional expenditure, directly impacting profitability.

War-Driven Slowdown

Mr. Chawla, further added that, “The automobile industry is absorbing costs temporarily, unable to immediately reflect them on end products, but suppliers are under pressure. We feel this should be a temporary phase, and once the war situation stabilises, supplies will normalise. India’s dependence on imports will worsen the problem, if the conflict escalates. The government is already urging reduced consumption and limiting single‑use plastics, except for essential medical equipment. For now, we have to wait and watch.”

Mr. Rambhia further added that, “It is very difficult to say what America will do tomorrow. Every day there is a change of direction. One week Donald Trump, President of the United States announces that the war is over, the next week he says it will intensify. With such flip‑flops, oil prices keep changing practically every week. Polymer prices are linked to oil, as about 4% of crude oil is converted to polymers. Because of this uncertainty, plastic processors are unwilling to book larger orders at fixed rates.

More than 50% of MSME production is running only partially. Jobs are affected, workers have migrated back to hometowns, and the industry is under huge stress. Government has released emergency aid financing, but uncertainty in supply remains. Plastic comes in hundreds of grades, and processors now spend hours hunting for material at reasonable prices.

Mr. Rambhia concluded stating that, “When the plastic processing industry is hit hard, new mould making takes a backseat. Projects are being held up, and price increases of 15–35% depending on grade and volume are common. Trust and cooperation between processors and end users is the only way forward. Transparency and patience are needed to survive this phase. India is better off percentage‑wise compared to smaller economies, but the absolute impact is large because of the scale of our economy. Injection moulding industry face huge impact, and demand for tooling in the short term will go down drastically. Even after the war ends, it will take months for things to return to normal.”

Key Report Takeaways

According to Mordor Intelligence- By end-user industry, the packaging sector led with a 57.12% India Engineering Plastics market share in 2025, while the electrical and electronics sector is projected to post the fastest growth of 8.55% CAGR (2026-2031). By resin type, polyethylene terephthalate (PET) accounted for a 58.22% share of the Indian Engineering Plastics market size in 2025, whereas fluoropolymer is anticipated to advance at a 9.12% CAGR between 2026 and 2031.

According to Mordor Intelligence, India’s engineering plastics demand is heavily concentrated in Gujarat, Maharashtra, and Tamil Nadu. In Gujarat, the Dahej-Vadodara corridor integrates essential components such as paraxylene, PTA, PET, and fluoropolymer chains, with the added advantage of port access at Hazira and Mundra. Notably, resin exports from Gujarat benefit from significant freight savings over inland plants, highlighting the state’s cost edge. Maharashtra’s Pune-Aurangabad-Mumbai triangle, a hub for automotive and electronics assemblers, sees a robust demand for PA 66, polycarbonate, and ABS. In Tamil Nadu, a center for EV production, smartphone assembly, and tire manufacturing, there is a surge in demand for glass-fiber-reinforced polyamide, flame-retardant ABS, and high-clarity polycarbonate. Bengaluru, supported by Tata Electronics and prominent IT hardware suppliers, drives the demand for high-performance resins such as LCP. Meanwhile, in Hyderabad’s Telangana corridor, fluoropolymers find their application in pharmaceutical equipment.