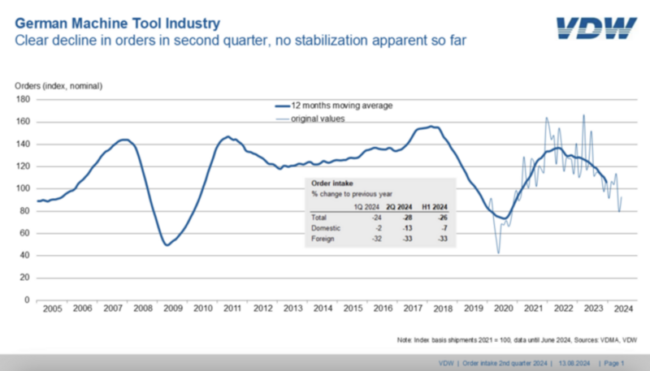

– Orders received by the German machine tool industry in the second quarter of 2024 were 28 percent down on the same period last year. Orders from Germany fell by 13 percent whereas those from abroad dropped by 33 percent. Orders received in the first half of 2024 were 26 percent down on the same period last year. Domestic orders were 7 percent lower. Orders from abroad were 33 percent below the previous year’s figure.

“The order volume is at its lowest level since Q4 2020,” sums up Dr. Markus Heering, Executive Director of the VDW (German Machine Tool Builders’ Association), Frankfurt am Main. “Orders from abroad fell significantly, whereas those from Germany held up better. However, this is not due to the hoped-for turnaround, but rather the result of a handful of project-based business deals,” continues Heering.

Overall, business levels are down across all customer sectors and markets. The picture was slightly brighter in individual sectors such as aviation, medical technology, power engineering and shipbuilding. Interest in electric vehicles is currently sluggish, as evidenced by the weak sales figures. Performing significantly better than the new machine business at present are service, components, repairs, maintenance and conversions. Automation remains a key driver in the sector.

Orders are not expected to stabilize to any great extent until the second half of 2024, with hopes being pinned on the final quarter in particular. Major industry trade fairs such as the AMB in Stuttgart, the IMTS in Chicago and the Jimtof in Tokyo could provide impetus here. Nevertheless, orders are expected to be significantly down in 2024 as a whole.

VDW’s forecasting partner Oxford Economics is expecting to see a distinct broad-based recovery in demand for machine tools across all regions in 2025 and 2026. The international market is predicted to pick up strongly again, however the momentum in Germany is expected to be significantly weaker.

“The forecast growth will not, however, be able to compensate for the losses from the last two years,” says Markus Heering. Previous peak values are still far from being matched. Foreign markets are almost back up to the 2018 levels in nominal terms, but domestic markets have lost ground for structural reasons, concludes the VDW Executive Director.

Sluggish new orders and the dwindling levels of orders on hand mean that the producers should resign themselves to significant reductions in the current year. A fall of 8 percent is forecast.